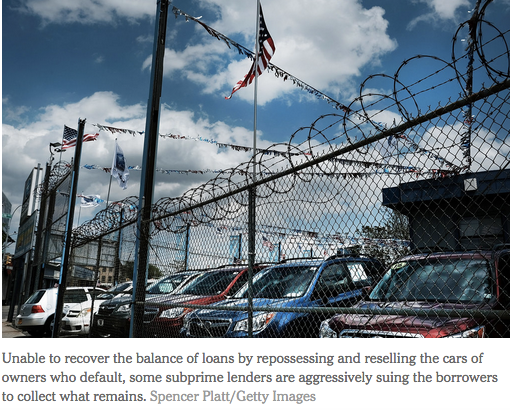

With their low credit scores, buying or leasing a new car is not an option. And when all the interest and fees of a subprime loan are added up, even a used car with mechanical defects and many miles on the odometer can end up costing more than a new car.

Subprime lenders are willing to take a chance on these risky borrowers because when they default, the lenders can repossess their cars and persuade judges in 46 states to give them the power to seize borrowers’ paychecks to cover the balance of the car loan.

Now, with defaults rising, federal banking regulators and economists are worried how the strain of these loans will spill over into the broader economy.

For low-income Americans, the fallout could, in some ways, be worse than the mortgage crisis.

With mortgages, people could turn in the keys to their house and walk away. But with auto debt, there is increasingly no exit. Repossession, rather than being the end, is just the beginning.